When grandparents want to help pay for their grandchildren’s education, a 529 college savings plan often comes to mind. It’s tax-advantaged, flexible, and shows a loving commitment to a child’s future. But here’s the question many families wrestle with: should grandparents own the 529 plan themselves, or should they contribute to a parent-owned account instead? The answer isn’t always straightforward. Despite its advantages, there are significant disadvantages of grandparents owning 529 plans that families need to understand before making this decision. From financial aid complications to control issues, the ownership structure matters more than most people realize.

In this guide, we’ll walk through everything you need to know about grandparents and 529 plans. The guide includes the potential pitfalls of grandparent ownership and smarter alternatives that might work better for your family.

What Is a 529 Plan? A Quick Overview

Before diving into the ownership question, let’s make sure we all understand what a 529 plan actually is.

A 529 plan is a tax-advantaged savings account designed specifically for education expenses. These plans are sponsored by states, state agencies, or educational institutions, and they come in two main types: college savings plans and prepaid tuition plans. Most families use the college savings plan version, which works similarly to a retirement account but for education.

The money you contribute grows tax-free. Withdrawals are also tax-free when used for qualified education expenses like tuition fees, books, room and board, and even K-12 tuition up to $10,000 per year. Many states also offer tax deductions or credits for contributions.

Anyone can open a 529 plan for the future student, including parents, grandparents, aunts, uncles, or even family friends. The person who opens and funds the account is called the account owner, and this designation carries important implications we’ll explore below.

Can Grandparents Contribute to a 529 Plan?

Can grandparents contribute to a 529 plan? Yes, and there are actually two ways they can do this:

Option 1: Open their own grandparent-owned 529 plan where they are the account owner and the grandchild is the beneficiary.

Option 2: Contribute to a parent-owned 529 plan, making gifts directly to the account that the parents control.

Both options are perfectly legal and come with the same tax benefits for the contributions. However, they have very different implications for financial aid, control, and estate planning. Understanding these differences is crucial for making the right choice for your family.

The Main Disadvantages of Grandparents Owning 529 Plans

While it might seem simpler for grandparents to open and manage their own 529 accounts, this approach comes with several significant drawbacks that can affect your grandchild’s college funding.

1. Financial Aid Impact (The Biggest Concern)

This is the most significant disadvantage of grandparents owning 529 plans, and it’s the reason many financial advisors recommend against this ownership structure.

Here’s how it works: When students complete the Free Application for Federal Student Aid (FAFSA), they must report assets and income. The FAFSA formula looks at this information to determine how much financial aid a student qualifies for through something called the Expected Family Contribution (EFC), now called the Student Aid Index (SAI).

The problem with grandparent-owned 529 plans:

Under current FAFSA rules, grandparent-owned 529 plans don’t need to be reported as an asset on the FAFSA. That sounds good, right? But here’s the catch: when grandparents take distributions from their 529 plan to pay for college expenses, that money counts as untaxed income to the student on the following year’s FAFSA.

Student income is assessed at a much higher rate than parent assets. Specifically, student income can reduce financial aid eligibility by up to 50% of the distribution amount. So if grandparents withdraw $10,000 from their 529 plan to help with freshman year expenses, it could reduce the student’s financial aid package by up to $5,000 for sophomore year.

This creates a difficult situation where the very act of helping pay for college can inadvertently reduce the financial aid the student receives, potentially making the net benefit much smaller than intended.

Important note: The FAFSA rules changed significantly with the 2024-2025 form (which applies to students starting college in fall 2024). Previously, the impact was even more severe. The current rules still create problems, but they’re somewhat less dramatic than before. However, financial aid rules can change, and families need to stay informed about current regulations.

2. Control and Flexibility Issues

When grandparents own a 529 plan, they maintain complete control over the account. While this might seem like an advantage (and we’ll discuss when it actually is), it can create complications.

Potential control issues include:

Family dynamics and disagreements: If there’s any family disagreement about education choices, grandparent control can become a source of conflict. What if the grandchild wants to attend a college the grandparents don’t approve of? What if parents and grandparents have different values about appropriate education spending?

Changing relationships: Life happens. Family relationships can become strained over time. If the relationship between grandparents and parents deteriorates, the grandparent might restrict access to funds, leaving the family in a difficult position.

Coordination challenges: When multiple 529 accounts exist for the same beneficiary, coordination becomes more complex. Parents might not know exactly how much grandparents have saved, making financial planning more difficult. This can lead to over-saving in some accounts and under-saving in others.

Limited parental oversight: Parents typically manage most aspects of their children’s education and finances. When grandparents own the 529, parents have no visibility over these education funds, which can make financial planning challenging.

3. Estate Planning Complications

Many grandparents choose to open 529 plans as part of their estate planning strategy, but grandparent-owned accounts can create unexpected complications.

The estate planning concerns:

Account ownership stays with the grandparent: Unlike some other gifting strategies, when you open a 529 plan, you remain the owner. This means the assets could potentially be subject to creditor claims against the grandparent in some situations.

What happens if the grandparent dies? Most 529 plans allow you to name a successor owner. If this isn’t properly documented, the account could end up in probate. This delays access to funds and could create tax complications.

Less effective for estate reduction: While 529 contributions do remove assets from your taxable estate (especially using the five-year gift tax averaging rule), grandparents maintain control over the assets. Some estate planning attorneys consider this a less clean transfer compared to gifting directly to a parent-owned account.

Potential for multiple accounts: If grandparents open separate 529 accounts for multiple grandchildren, managing all these accounts as they age can become burdensome. Simplifying estate planning becomes harder with numerous separate accounts.

4. State Tax Benefit Limitations

Many states offer tax deductions or credits for 529 plan contributions, but these benefits often come with strings attached.

State residency matters: Some states only allow tax deductions for contributions to their own state’s 529 plan. If grandparents live in a different state from the parents or grandchild, they might not receive the same tax benefits.

Contribution limits for deductions: States cap how much you can deduct annually. If grandparents want to make a large, one-time contribution, they might not receive the full tax benefit that year.

Who gets the benefit? When grandparents own the 529, only they can claim the state tax deduction (if available). If the parents are in a higher tax bracket or have more state income tax liability, the family might benefit more from parents claiming the deduction instead.

5. Reduced Transparency for the Family

Among the disadvantages of grandparents owning 529 plans is a lack of simple communication and transparency. Transparency issues include:

Parents don’t know the account balance: Unless grandparents regularly share statements, parents may not know how much money is saved for the kids. This makes it difficult to plan appropriately for college costs.

Uncertainty about distribution timing: Parents might not know when or how grandparents plan to use the funds, making it hard to coordinate financial aid strategies, student loans, or other funding sources.

Difficulty optimizing tax strategies: Without full visibility into all education funding sources, families can’t optimize their tax strategies across all accounts.

Advantages and Disadvantages of Grandparents Owning 529 Plans: The Full Picture

To make an informed decision, let’s look at both sides. While we’ve focused on the disadvantages, there are situations where grandparent ownership makes sense.

| Advantages | Disadvantages |

| Grandparents maintain complete control over funds | Distributions count as student income on FAFSA, potentially reducing financial aid by up to 50% |

| Can prevent parents from misusing education funds | Creates coordination challenges between family members |

| Useful if concerned about parental financial responsibility | Complicates estate planning and probate situations |

| May protect assets in case of parental divorce | Reduces transparency and makes comprehensive planning difficult |

| Provides grandparents satisfaction of direct involvement | May limit state tax benefits depending on residency |

| Can change beneficiary if original beneficiary doesn’t attend college | Less flexibility for parents managing overall education strategy |

Better Alternative: Grandparents Gifting to 529 Plans Owned by Parents

For most families, a smarter strategy is grandparents gifting to 529 plans that are owned by the parents. This approach combines the generosity of grandparent contributions with better financial aid treatment and family coordination.

How this works:

Instead of opening their own 529 account, grandparents simply make contributions to the 529 plan already established by the parents. Most 529 plans make this easy, providing gift contribution forms or online portals where anyone can contribute.

The advantages of this approach:

Better financial aid treatment: Parent-owned 529 plans are assessed as parent assets on the FAFSA, which has a much lower impact on financial aid (maximum 5.64% assessment rate) compared to the 50% assessment rate for student income from grandparent-owned accounts.

Improved coordination: Everyone knows where all the education money is, making planning easier and preventing duplication or gaps in coverage.

Simplified estate planning: The gift is a completed transfer out of the grandparent’s estate with no ongoing management responsibility.

Maintains family harmony: Parents retain appropriate control over their child’s education while still receiving generous support from grandparents.

Easier account management: One account is simpler to manage than multiple accounts, especially when dealing with investment choices and rebalancing.

Gift Tax and 529 Plans: What Grandparents Need to Know

When we talk about grandparents contributing to 529 plans, whether they own the account or contribute to a parent-owned one, we need to address 529 plan gift tax implications.

The good news is that 529 contributions are treated as completed gifts for tax purposes, which means they come with some favorable tax treatment.

The basic gift tax rules:

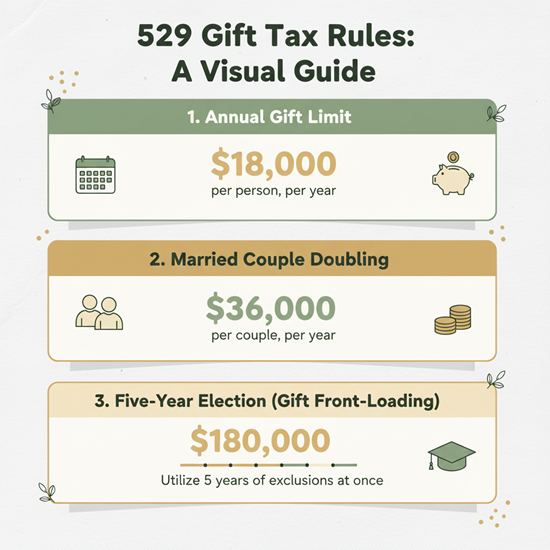

Annual gift tax exclusion: For 2024, you can give up to $18,000 per person per year without any gift tax implications or reporting requirements. Since each grandparent is a separate person, a married couple can jointly give $36,000 per grandchild per year.

Five-year election for 529 contributions: Here’s where 529 plans offer something special. You can make up to five years’ worth of annual exclusion gifts at once to a 529 plan and spread it over five years for gift tax purposes. This means a married couple could contribute up to $180,000 per grandchild in one year (5 years × $36,000) without triggering gift tax.

How this works for both ownership structures: These gift tax rules apply whether grandparents open their own 529 plan or contribute to a parent-owned account. The tax advantages are identical.

Important considerations:

If you use the five-year election and then make another gift to the same beneficiary during that five-year period, it could trigger gift tax reporting requirements. You also need to file Form 709 (Gift Tax Return) to report the five-year election, even though no tax is due.

If you die during the five years after making the accelerated contribution, a prorated portion of the contribution is pulled back into your estate for estate tax purposes.

When Grandparent-Owned 529 Plans DO Make Sense

Despite the disadvantages we’ve discussed, there are specific situations where grandparents owning 529 plans can be the right choice.

Consider grandparent ownership if:

Your grandchild won’t qualify for need-based aid anyway: If the family’s income and assets are high enough that they won’t receive financial aid regardless, the FAFSA impact of grandparent-owned 529s becomes irrelevant. For high-income families, grandparent ownership provides control benefits without the financial aid downside.

You have concerns about parental financial responsibility: If you’re worried that parents might misuse funds intended for education, maintaining ownership protects your contribution. This is delicate territory, but it’s a real concern for some families.

There are complicated family situations: In cases of divorce, remarriage, or strained family relationships, grandparent ownership might provide more stability and ensure funds are used as intended.

You want to maintain control for multiple grandchildren: If you have several grandchildren and want the flexibility to shift funds between them based on need, ownership gives you that control. You can change the beneficiary on a 529 plan you own.

The timing strategy: If you plan to delay distributions until the last years of college (junior and senior year) or graduate school, the financial aid impact is minimized since there are fewer subsequent years of FAFSA forms affected.

You’re comfortable with complex planning: Some families work with financial advisors to time grandparent 529 distributions strategically or coordinate with other financial aid planning techniques to minimize negative impacts.

Practical Action Steps for Grandparents and Parents

So what should your family actually do? Here’s a practical roadmap for making this decision and implementing the right strategy.

For grandparents who want to help:

Step 1:

Have an honest conversation with your grandchildren’s parents. Discuss their financial situation, education savings plans, and whether need-based financial aid is likely to be important.

Step 2:

Consider contributing to a parent-owned 529 plan as your default strategy, unless specific circumstances suggest otherwise.

Step 3:

If you do open your own account, work with a financial advisor to understand the timing strategies that can minimize financial aid impact.

Step 4:

Document everything clearly. Make sure there’s a successor owner named, and communicate your plans clearly to avoid surprises.

Step 5:

Review your decision periodically. Financial aid rules change, family circumstances evolve, and what makes sense today might need adjustment in the future.

For parents:

Step 1:

Open a 529 plan early if you haven’t already, even if you can only contribute small amounts. This creates a vehicle for grandparent contributions.

Step 2:

Make it easy for grandparents to contribute by providing account information and explaining how to make contributions.

Step 3:

Communicate regularly about college savings progress and plans. Transparency helps everyone make better decisions. Involve the kids in those money conversations in age-appropriate ways.

Step 4:

If grandparents insist on owning their own 529, work together on timing strategies and understand how it will affect your financial aid planning.

Step 5:

Consider whether financial aid is likely to be a factor for your family. If your income is high enough to disqualify you from need-based aid, the disadvantages of grandparent-owned accounts become much less relevant.

The Bottom Line: How to Avoid the Disadvantages of Grandparents Owning 529 Plans

Understanding the disadvantages of grandparents owning 529 plans is essential for making informed decisions about education funding. While grandparent contributions are generous and valuable, the ownership structure matters significantly.

For most families, grandparents contributing to parent-owned 529 plans offers the best combination of tax benefits, financial aid treatment, and family coordination. This approach maximizes the benefit of grandparent generosity while minimizing potential downsides.

However, every family is different. High-income families who won’t qualify for financial aid, families with complicated dynamics, or situations where control is paramount might find that grandparent-owned accounts make more sense despite the disadvantages.

As with any important decision, being financially literate and up to date is always advised. The key is to make an informed, intentional decision rather than simply defaulting to one approach because it seems simpler. Talk openly with your family, consider working with a financial advisor who understands education planning, and remember that the goal is the same regardless of account ownership: helping the next generation access quality education without unnecessary financial burden.

Whatever you decide, the fact that you’re thinking carefully about these issues means you’re already on the right track. Education funding requires planning, coordination, and sometimes compromise, but with good communication and understanding of the options, your family can create a strategy that works for everyone involved.

**Disclaimer:** The information provided in this article is for educational and informational purposes only and should not be construed as financial, tax, or legal advice. Every family’s situation is unique, and 529 plan strategies involve complex financial aid, tax, and estate planning considerations. Before making any decisions about education funding, we recommend consulting with a qualified financial advisor, tax professional, or estate planning attorney who can provide personalized guidance based on your specific circumstances.